By Tom Anderson, CNBC–

“It has less detail than the plan released by the Trump campaign,” said Scott Greenberg, an analyst at the Center for Federal Tax Policy at the Tax Foundation.

Here’s what we know:

Trump’s revised proposal would reduce the current seven tax brackets to three with rates of 10 percent, 25 percent and 35 percent.

Those rates are slightly different than those Trump proposed during the campaign. The new plan increases the top rate to 35 percent from 33 percent in the old plan and lowers the bottom rate to 10 percent, from 12 percent in the old plan.

The one-page plan doesn’t spell out exactly where each tax bracket will fall like his original tax proposal.

Standard deductions

The standard deduction would nearly double under Trump’s proposal, but it’s less than what he offered during the campaign.

“We are going to double the standard deduction so a married couple wouldn’t pay any taxes on the first $24,000 income they earn. So in essence, we are creating a zero tax rate — yes, a zero tax rate — for the first $24,000 that a couple earns,” said Gary Cohn, head of Trump’s National Economic Council, during the news conference rolling out the new plan.

For 2017, the standard deduction for single filers is $6,350 and $12,700 for married couples filing jointly. During the campaign, Trump had proposed increasing the standard deduction to $15,000 for single filers and to $30,000 for married joint filers.

Itemized deductions

Initially, Trump proposed capping itemized deductions at $100,000 for single filers and $200,000 for married couples filing jointly. The new plan doesn’t talk about caps except to say the administration wants to “

Under the new plan, tax breaks for charitable giving, mortgage interest and retirement savings would remain in place. However, the administration now wants to eliminate the deduction for state and local taxes.

Known as the SALT deduction, it is one of the largest federal tax expenditures, with an estimated revenue cost of $96 billion in 2017 and $1.3 trillion over the 10-year period from 2017 to 2026, according to the Tax Policy Center.

More than half of taxpayers who are earning $75,000 and above claim SALT deductions on their federal income tax returns as do more than 90 percent of taxpayers who make $200,000 or more. (See chart below.)

Ending the SALT deduction would affect people in states with relatively high state and local taxes.

Alternative minimum tax

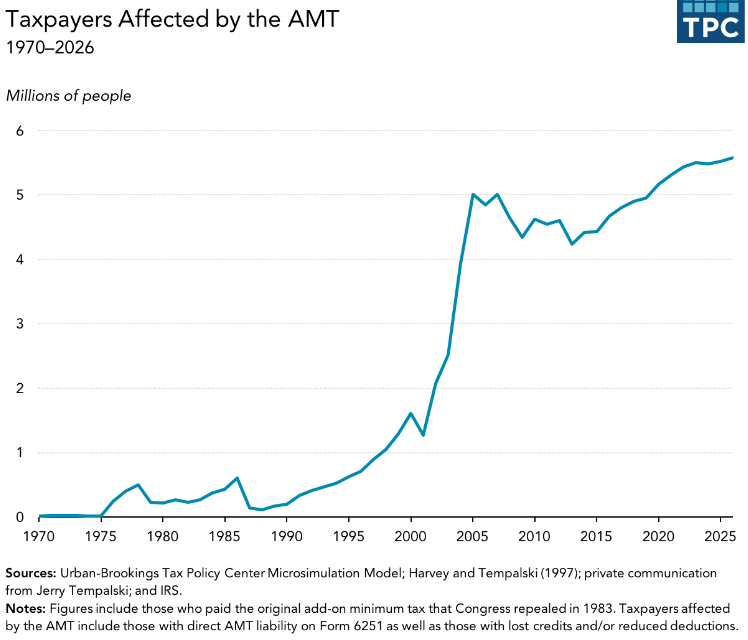

The Trump administration remains committed to ending the alternative minimum tax, known as the AMT. It requires more than 5 million taxpayers to calculate their liability twice and then pay the higher amount. It used to apply only to wealthy taxpaypers, but the AMT is not indexed to inflation. (See chart below.)

“AMT possibly going away is a big deal,” said Howard Wagner, managing director at Crowe National Tax Services.

High earners are limited in receiving the benefits of the SALT deduction, which the new Trump tax plan would end, because of the AMT. So ending the SALT deduction and the AMT may offset each other. “You’re really not losing something if you don’t benefit from the deduction,” Wagner said.

Capital gains taxes

The Trump administration continues to push to eliminate the 3.8 percent net income investment tax created by the Affordable Care Act.

The tax applies to investment income of taxpayers with a modified adjusted gross income of more than $200,000 for single filers and $250,000 for married couples filing jointly. Ending the net income investment tax would drop the effective capital gains tax rate for high earners from 23.8 percent to 20 percent.

Investors who are selling property or securities this year should consider the tax consequences of postponing those transactions because they may possibly take advantage of lower capital gains rates in the future, Wagner said.

Next steps

Lawmakers will have to turn Trump’s outline of tax reform into legislation.

The Tax Foundation’s Greenberg said the next major step in the debate will be looking at legislative language from the House Ways and Means Committee.

Republican Rep. Kevin Brady, chairman of that committee, told CNBC’s “Squawk Box” on Thursday that there’s “80 percent common ground” with the White House on the new tax reform plan. Of course, Brady said the same thing in December.

Leave A Comment

You must be logged in to post a comment.